Elasticity of supply shows how sensitive producers are to a change in price. The elasticity of supply is based on time limitations. Essentially, similar to how customers respond to price changes, producers need time to produce more.

- Elastic Supply:

- Producers are highly responsive to price changes.

- The supply curve is flatter.

- Typically applies in the long-run, as producers have more time to adjust

- For example, manufactured goods like cars or electronics.

- Inelastic Supply:

- Producers are less responsive to price changes.

- The supply curve is steeper.

- Common in the short-run, when production adjustments are limited.

- For example, agricultural goods (e.g., crops) during a growing season.

- Perfectly Inelastic Supply:

- Quantity supplied does not change, regardless of price.

- Represented by a vertical line.

- For example, fixed supply goods, like unique artworks or land in a specific location.

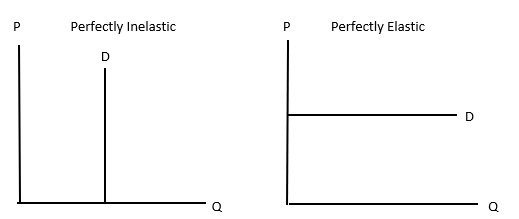

Perfectly inelastic is when the Q doesn’t change (vertical line) and perfectly elastic is a horizontal line. See:

Determinants of Elasticity of Supply

- Time Horizon:

- Short-Run: Supply is usually inelastic due to limited production flexibility.

- Long-Run: Supply becomes more elastic as firms can adjust resources and production.

- Flexibility of Production:

- Goods that can be produced quickly and cheaply are more elastic.

- For example, t-shirts vs. heavy machinery

- Availability of Inputs:

- Easy access to raw materials makes supply more elastic.

- For example, abundant wood supply allows quick production of furniture.

- Storage Capabilities:

- Goods that can be stored are more elastic since producers can respond to price changes by releasing inventory.

- For example, non-perishable goods like canned food.

See also: 1.5 — Cost-Benefit Analysis and 3.6 — Short-Run and Long-Run Decision-Making.