The production function describes how inputs (like labour and capital) are transformed into outputs. It shows the relationship between resource use and production.

Definitions

- Inputs: Materials (factors) used to produce outputs, as described in 1.2 — Resource Allocation and Economic Systems

- Outputs: Firms must produce output to earn a profit

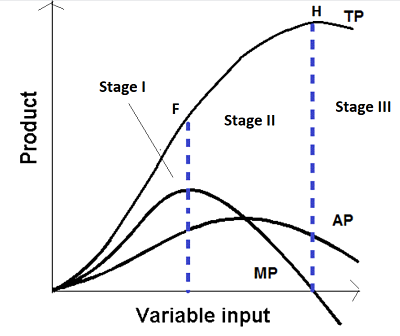

- Total Physical Product (TP): Total output or quantity produced

- Marginal Product (MP): Additional output created by additional input (workers)

- Average Product (AP): Output per unit of input

- Fixed Resource: Doesn’t change

- Accounting Profit: Total revenue accounting for only explicit costs

- Economic Profit: Total Revenue accounting for both impge, forgone rent, etc.

The difference between accounting and economic profit is further described in 3.4 — Types of Profit.

Law of Diminishing Marginal Returns

When more units of a variable input (e.g., labor) are added to a fixed input (e.g., land or machinery), the additional output () eventually decreases. This occurs because fixed inputs limit productivity as more variable inputs are added.

These theories are quite similar to 1.5 — Cost-Benefit Analysis and 1.6 — Marginal Analysis and Consumer Choice. The idea of diminishing returns is also similar to the Law of Diminishing Marginal Utility, as described in 1.4 — Demand.

Correspondingly, there are three stages of marginal returns:

- Stage 1: Increasing Marginal Returns

- : Marginal product rises due to better utilization of inputs (e.g., specialization).

- Total product grows at an increasing rate.

- Stage 2: Diminishing Marginal Returns

- : Each additional input adds less to total output.

- Total product grows at a decreasing rate.

- Stage 3: Negative Marginal Returns

- : Adding more input decreases total output due to inefficiencies (e.g., overcrowding).

Relationships Between TP, MP, and AP

- TP increases as long as , but the rate of increase slows when begins to decline